What is KYC?

KYC, or Know Your Customer, KYC Process is a crucial aspect of any business that deals with financial transactions. It refers to the process of verifying the identity of customers or clients and assessing their potential risks and fraudulence.

What is the meaning of KYC?

KYC stands for Know Your Customer. KYC services are used by businesses use to verify and collect information about their customers, clients, or counterparties. This process involves identifying and verifying the identity of the customer, assessing their risks and fraudulence, and complying with regulatory requirements.

KYC regulations were introduced by regulatory bodies to combat money laundering, terrorist financing, and other illegal activities. These regulations require businesses to collect and verify customer information such as name, address, date of birth, and identification documents such as a passport or driver’s license.

The KYC process involves several steps, including customer identification, risk assessment, customer due diligence, and ongoing monitoring of transactions. The goal of these steps is to ensure that the business is not unwittingly involved in any illegal activities and to protect the company’s reputation and assets.

The KYC process is particularly crucial in industries such as banking, insurance, and investment management, where large amounts of money are being transacted regularly. However, it is also becoming increasingly important in other sectors, such as e-commerce and online payment systems.

Non-compliance with KYC regulations can lead to severe consequences, including legal penalties, fines, and damage to a company’s reputation. Therefore, businesses must ensure that they have robust KYC procedures in place to comply with the regulations and protect themselves from potential risks.

What is KYC Document?

KYC documents refer to the various documents that are required by businesses to verify the identity of their customers or clients. These documents typically include proof of identity, proof of address, and other relevant information that is necessary for compliance with KYC regulations.

Proof of identity documents may include a passport, driver’s license, or national identity card. These documents typically include a photograph, name, date of birth, and other identifying information. Proof of address documents may include a utility bill, bank statement, or rental agreement that shows the customer’s current address.

In addition to these documents, businesses may also require other information from their customers, such as their occupation, source of income, and tax identification number. This information is used to assess the customer’s risk profile and comply with regulatory requirements.

The KYC document requirements may vary depending on the industry and the specific regulations that apply. For example, banks may require additional information from their customers, such as information about their financial transactions and investments.

The purpose of KYC documents is to ensure that businesses are not unwittingly involved in illegal activities such as money laundering and terrorist financing. By collecting and verifying customer information, businesses can assess the risks associated with each customer and take appropriate measures to mitigate those risks.

What is KYC in Banking?

AML KYC stands for Anti-Money Laundering and Know Your Customer. It is a set of regulations that require financial institutions and other regulated entities to verify and identify their customers, assess the risk of money laundering and terrorist financing, and report suspicious activities to the authorities.

The AML KYC regulations are designed to prevent criminals from using the financial system to launder money or finance terrorist activities. These regulations require businesses to collect and verify customer information such as name, address, date of birth, and identification documents such as a passport or driver’s license.

The KYC process involves several steps, including customer identification, risk assessment, customer due diligence, and ongoing monitoring of transactions. The AML component requires businesses to monitor transactions for suspicious activities, report suspicious activities to the authorities, and maintain appropriate records.

Non-compliance with AML KYC regulations can lead to severe consequences, including legal penalties, fines, and damage to a company’s reputation. Therefore, businesses must ensure that they have robust AML KYC procedures in place to comply with the regulations and protect themselves from potential risks.

What is Video KYC?

Video KYC refers to the process of conducting a Know Your Customer (KYC) verification remotely through a video call. This process allows businesses to verify the identity of their customers in a more efficient and convenient manner while complying with regulatory requirements.

The video KYC process typically involves the customer providing their identification documents, such as a passport or driver’s license, and answering a series of questions to confirm their identity. A trained KYC professional conducts the video call, verifies the documents and information provided, and assesses the potential risks associated with the customer.

Video KYC is becoming increasingly popular, especially in the financial services industry, as it allows for a more streamlined and cost-effective process than traditional KYC methods. It also enables businesses to reach a wider audience and expand their customer base beyond their physical locations.

Video KYC has become even more relevant during the COVID-19 pandemic as it allows businesses to conduct KYC verification without the need for in-person meetings, reducing the risk of transmission and ensuring social distancing protocols are maintained.

However, businesses must ensure that they have robust security measures in place to protect against fraudulent activities such as deepfakes, where someone may attempt to impersonate the customer in the video call. Therefore, businesses should consider using advanced technologies such as biometric verification and facial recognition to enhance the security of the video KYC process.

What is OVD in KYC?

OVD in KYC stands for Officially Valid Document. An OVD is a document that is issued by a government authority and is recognized as a valid proof of identity and address. It is one of the essential documents that are required to complete the KYC process.

OVDs are typically issued by government agencies such as the Passport Office, Election Commission, and the Income Tax Department. Examples of OVDs include a passport, a driver’s license, a voter ID card, a PAN card, or a Aadhaar card.

During the KYC process, businesses verify the authenticity of the OVD provided by the customer. They cross-check the information provided in the OVD with other documents and databases to ensure that the customer is who they claim to be.

The use of OVDs in KYC helps to prevent identity theft, fraud, and other financial crimes. It also ensures that businesses comply with regulatory requirements and maintain the integrity of the financial system.

It is essential to note that businesses may require additional documents and information depending on the type of account, the customer’s profile, and the applicable regulations. For instance, a bank may require additional documents such as a recent utility bill or a bank statement as proof of address.

Why is KYC Important?

KYC verification is the process of verifying the identity of a customer and assessing their potential risk of financial crimes such as money laundering, terrorism financing, or fraud. KYC stands for “Know Your Customer,” and it is a critical part of the compliance process for businesses in the financial sector and other regulated industries.

The KYC verification process typically involves collecting information from the customer, such as their name, address, date of birth, and identification documents such as a passport or driver’s license. Businesses then verify this information using reliable sources such as government databases, credit bureaus, and third-party KYC service providers.

The KYC verification process aims to ensure that businesses have a complete and accurate understanding of their customers’ identities, their financial activities, and their potential risks. This helps to prevent financial crimes and protect the integrity of the financial system.

KYC verification is not a one-time process; it is an ongoing process that requires businesses to monitor their customers’ activities and update their information regularly. This helps businesses to identify any suspicious activities and report them to the relevant authorities.

In recent years, the KYC verification process has evolved significantly, and businesses have adopted innovative technologies such as biometric authentication and artificial intelligence to improve the accuracy and efficiency of the process. These technologies have helped businesses to streamline the KYC verification process, reduce costs, and improve the customer experience.

What is eKYC?

eKYC stands for electronic Know Your Customer. It is a process of verifying the identity of customers electronically, without the need for physical documents and in-person verification. eKYC is a convenient and efficient way for businesses to complete the KYC process and onboard new customers remotely.

The eKYC process typically involves the customer providing their personal information such as name, address, and identification details through a digital platform or mobile application. The information is then validated using reliable sources such as government databases, credit bureaus, or third-party KYC service providers.

eKYC uses advanced technologies such as biometric verification and facial recognition to authenticate the customer’s identity, which reduces the risk of fraud and improves the accuracy of the process. Biometric verification can be done using fingerprints, iris scan, or face recognition, depending on the level of security required.

eKYC is becoming increasingly popular, especially in the financial services industry, as it allows businesses to onboard new customers quickly and efficiently while complying with regulatory requirements. It also improves the customer experience by reducing the time and effort required to complete the KYC process.

However, businesses must ensure that they have robust security measures in place to protect against data breaches and fraudulent activities. They must comply with data protection and privacy laws and ensure that customer information is kept secure and confidential.

Why is KYC required?

KYC (Know Your Customer) is an essential process for businesses in the financial sector and other regulated industries. The importance of KYC lies in its ability to help businesses prevent financial crimes such as money laundering, terrorism financing, fraud, and other illicit activities.

Here are some reasons why KYC is important:

- Compliance with regulations: KYC is a legal requirement for businesses operating in the financial sector and other regulated industries. Compliance with KYC regulations helps businesses avoid legal penalties, reputational damage, and loss of license.

- Prevention of financial crimes: KYC helps businesses to identify and prevent financial crimes such as money laundering, terrorism financing, and fraud. By verifying the identity of their customers, businesses can detect any suspicious activities and report them to the relevant authorities.

- Protection of the financial system: KYC helps to protect the integrity of the financial system by preventing illicit activities that could undermine its stability. KYC ensures that only legitimate customers are onboarded, and their financial transactions are monitored for any suspicious activities.

- Better risk management: KYC enables businesses to assess the risk level of their customers and determine the appropriate level of due diligence required for each customer. This helps businesses to allocate their resources efficiently and reduce their exposure to risk.

- Improved customer experience: KYC helps to streamline the onboarding process for customers, reducing the time and effort required to open an account or access services. This improves the customer experience and helps businesses to retain their customers.

What is KYC Process?

KYC (Know Your Customer) is a process used by businesses to verify the identity of their customers and assess their risk level. The KYC process involves gathering personal and financial information from customers and verifying it against reliable sources. Here are the steps involved in the KYC process:

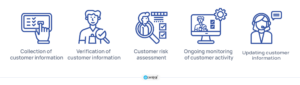

- Collection of customer information: The first step in the KYC process is to collect information from the customer. This information may include personal details such as name, address, date of birth, and identification documents such as passport or driving license. The business may also collect financial information such as income, assets, and source of funds.

- Verification of customer information: Once the customer information is collected, it is verified against reliable sources. This may include checking government databases, credit bureaus, or third-party KYC service providers. The verification process is designed to ensure that the customer’s information is accurate and reliable.

- Customer risk assessment: The next step is to assess the customer’s risk level. This is based on factors such as their source of income, the nature of their business, and their geographic location. The risk assessment is used to determine the appropriate level of due diligence required for each customer.

- Ongoing monitoring of customer activity: Once the customer is onboarded, their financial transactions are monitored for any suspicious activity. This helps businesses to detect and prevent financial crimes such as money laundering and terrorism financing.

- Updating customer information: The KYC process is an ongoing process, and businesses must update their customer information regularly. This includes verifying any changes to the customer’s personal or financial information.

How to perform KYC Online?

Performing KYC (Know Your Customer) online has become a popular way for businesses to onboard new customers and verify their identity. Here are the steps involved in performing KYC online:

- Collect customer information: The first step is to collect the customer’s personal and financial information. This may include their name, address, date of birth, and identification documents such as passport or driving license. The customer may be required to upload scanned copies of their identification documents.

- Verify customer information: Once the customer information is collected, it is verified against reliable sources. This may include checking government databases, credit bureaus, or third-party KYC service providers. The verification process is designed to ensure that the customer’s information is accurate and reliable.

- Customer identity verification: To verify the customer’s identity, the business may use various methods such as video KYC, biometric authentication, or electronic signatures. Video KYC involves conducting a live video call with the customer, where they are asked to display their identification documents and answer a series of questions. Biometric authentication involves using the customer’s fingerprints or facial recognition to verify their identity. Electronic signatures are used to obtain the customer’s consent and agreement to the terms and conditions of the service.

- Ongoing monitoring of customer activity: Once the customer is onboarded, their financial transactions are monitored for any suspicious activity. This helps businesses to detect and prevent financial crimes such as money laundering and terrorism financing.

Performing KYC online offers several benefits such as convenience, speed, and cost-effectiveness. However, businesses must ensure that their online KYC processes are compliant with regulatory requirements and secure to protect customer data.

How to perform KYC Verification Online?

Performing KYC (Know Your Customer) verification online is a crucial process for businesses to onboard new customers, verify their identity, and perform various types of verifications to ensure the authenticity of their personal and financial information. Here are the steps involved in performing KYC verification online:

- Collect customer information: The first step is to collect the customer’s personal and financial information. This may include their name, address, date of birth, and identification documents such as passport or driving license. The customer may be required to upload scanned copies of their identification documents for ID verification.

- Verify customer information: Once the customer information is collected, it is verified against reliable sources. This may include checking government databases, credit bureaus, or third-party KYC service providers. The verification process is designed to ensure that the customer’s information is accurate and reliable.

- Customer identity verification: To verify the customer’s identity, the business may use various methods such as video KYC, biometric authentication, or electronic signatures. Video KYC involves conducting a live video call with the customer, where they are asked to display their identification documents for face match and answer a series of questions. Biometric authentication involves using the customer’s fingerprints or facial recognition to verify their identity. Electronic signatures are used to obtain the customer’s consent and agreement to the terms and conditions of the service.

- Document verification: In addition to verifying the customer’s identity, the business may also need to verify their documents. This involves checking the authenticity of the customer’s identification documents using advanced document verification software for KYC verification and ID verification.

- Ongoing monitoring of customer activity: Once the customer is onboarded, their financial transactions are monitored for any suspicious activity. This helps businesses to detect and prevent financial crimes such as money laundering and terrorism financing.

Performing KYC verification online offers several benefits such as convenience, speed, and cost-effectiveness. However, businesses must ensure that their online KYC verification processes are compliant with regulatory requirements and secure to protect customer data.

What is KYC in the Banking Sector?

What are KYC requirements?

KYC, which stands for Know Your Customer, is a process that banks use to verify the identity of their customers. It is a regulatory requirement aimed at preventing financial crimes such as money laundering and terrorism financing. During the KYC process, banks collect personal and financial information from their customers and verify it against reliable sources. This information includes the customer’s name, address, date of birth, occupation, and identification documents such as a passport or driver’s license. Banks may also use various methods such as video KYC, biometric authentication, or electronic signatures to verify the identity of their customers. KYC in banking is essential to comply with regulations, prevent financial crimes, and maintain the bank’s reputation.

In banking, the KYC process involves collecting personal and financial information from customers and verifying it against reliable sources. This may include checking government databases, credit bureaus, or third-party KYC service providers. Banks may also use various methods such as video KYC, biometric authentication, or electronic signatures to verify the identity of their customers.

The KYC process is designed to ensure that the bank knows who their customers are, what their financial activities are, and whether they pose any risk to the bank or the wider financial system. Banks are required to perform KYC checks when a new account is opened, when there is a change in customer information, and when there are suspicious transactions.

The information collected during the KYC process includes the customer’s name, address, date of birth, occupation, source of income, and identification documents such as passport or driving license. The customer may be required to provide additional information such as the purpose of the account and the expected transaction volumes.

KYC in banking is a critical process that helps banks to comply with regulatory requirements, protect themselves and their customers from financial crimes, and maintain their reputation. Failure to comply with KYC regulations can result in severe penalties, including fines and loss of license.

What is KYC process in Banking?

eKYC, or digital KYC, is a process used in banking for onboarding new customers by verifying their identity electronically. It involves the use of digital technologies such as biometric authentication, digital signatures, and online identity verification services. With the increasing use of digital channels for banking, eKYC has become a popular and convenient way for customers to complete the KYC process.

eKYC can be done through a variety of methods such as facial recognition, fingerprint scanning, or iris scanning, depending on the bank’s preferred approach. This allows for a quick and seamless onboarding experience for the customer, without the need for physical documents or visits to the bank.

Moreover, the eKYC process can be automated using KYC APIs, which provide a standardized and secure method for sharing KYC data between banks and third-party verification providers. This allows banks to streamline their KYC processes, reduce costs, and improve the customer experience.

eKYC has become increasingly popular in recent years, particularly with the rise of digital banking and online account opening. It offers several benefits, including reduced processing times, enhanced security, and improved compliance with regulatory requirements. With the use of eKYC, banks can efficiently and securely onboard new customers while maintaining high levels of accuracy and compliance.

Why KYC is important in banking?

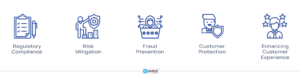

KYC, which stands for Know Your Customer, is a crucial process in banking that helps banks verify the identity of their customers and ensure that they are not involved in any fraudulent or illegal activities. Here are some reasons why KYC is important in banking:

- Regulatory Compliance: KYC is a regulatory requirement that banks must comply with. Financial regulators require banks to collect and verify the identity of their customers to prevent money laundering, terrorism financing, and other financial crimes.

- Risk Mitigation: KYC helps banks identify high-risk customers who may pose a risk to the bank’s reputation or financial stability. Banks can use KYC information to assess the risk of a customer and take necessary measures to mitigate the risk.

- Fraud Prevention: KYC helps banks prevent fraud by verifying the identity of their customers and detecting any inconsistencies or suspicious activity. Banks can use KYC information to monitor customer transactions and flag any unusual activity.

- Customer Protection: KYC helps protect customers from identity theft and other fraudulent activities. By verifying the identity of customers, banks can ensure that their personal and financial information is secure and protected.

- Enhancing Customer Experience: KYC helps banks provide a better customer experience by enabling them to offer customized products and services that meet their customers’ needs. By collecting and analyzing customer data, banks can gain insights into their customers’ behavior and preferences.

KYC APIs

What is KYC API?

KYC API is an application programming interface that enables businesses to perform identity verification and KYC checks on their customers electronically.

How does KYC API work?

KYC API works by integrating with third-party identity verification providers and enabling businesses to perform KYC checks on their customers using their services.

What are the benefits of using KYC API?

The benefits of using KYC API include faster processing times, reduced costs, enhanced security, and improved compliance with regulatory requirements.

Which companies provide KYC API services?

Several companies provide KYC API services, including IDcentral and many more.

What is the cost of using KYC API?

The cost of using KYC API varies depending on the provider, the number of verifications required, and the level of service needed.

How secure is KYC API?

KYC API is generally considered secure, as it uses encryption and other security measures to protect customer data.

What are the technical requirements for integrating KYC API?

The technical requirements for integrating KYC API vary depending on the provider and the technology used.

What documents are required for KYC verification using API?

The documents required for KYC verification using API may include government-issued IDs, proof of address, and other documents

How long does it take to integrate KYC API?

The time it takes to integrate KYC API depends on the complexity of the system and the level of customization required.

How reliable is KYC API for identity verification?

Aadhaar KYC API

What is Aadhaar KYC API?

Aadhaar KYC API is an interface provided by the Unique Identification Authority of India (UIDAI) that enables businesses to perform Aadhaar-based KYC checks on their customers.

How does Aadhaar KYC API work?

Aadhaar KYC API works by enabling businesses to capture Aadhaar numbers and biometric data of their customers, and then sending this data to UIDAI for verification. UIDAI then sends back a response indicating whether the customer’s details match their Aadhaar records.

What are the benefits of using Aadhaar KYC API?

The benefits of using Aadhaar KYC API include faster processing times, improved accuracy, reduced costs, and enhanced security.

What documents are required for Aadhaar KYC verification using API?

To perform Aadhaar KYC verification using API, businesses are required to capture the customer’s Aadhaar number and biometric data (fingerprint, iris scan, or face recognition).

Is Aadhaar KYC API secure?

Yes, Aadhaar KYC API is considered secure, as it uses encryption and other security measures to protect customer data.

What are the technical requirements for integrating Aadhaar KYC API?

The technical requirements for integrating Aadhaar KYC API vary depending on the provider and the technology used. However, businesses are required to comply with UIDAI’s guidelines and standards for using Aadhaar-based services.

What is the cost of using Aadhaar KYC API?

The cost of using Aadhaar KYC API varies depending on the provider and the level of service required.

Who can use Aadhaar KYC API?

Any business that is authorized to perform Aadhaar-based services can use Aadhaar KYC API. However, they must comply with UIDAI’s guidelines and standards for using Aadhaar-based services.

How reliable is Aadhaar KYC API for identity verification?

Aadhaar KYC API is generally reliable for identity verification, but it is important to choose a reputable provider and ensure that the system is properly configured to meet regulatory requirements.

What are the regulatory requirements for using Aadhaar KYC API?

Businesses are required to comply with UIDAI’s guidelines and standards for using Aadhaar-based services, as well as any other applicable regulations and laws.

KYC Check API

What is KYC Check API?

KYC Check API is an interface that allows businesses to perform KYC checks on their customers using automated processes and data sources.

How does KYC Check API work?

KYC Check API works by integrating with various data sources and using algorithms and machine learning to verify customer identities and perform KYC checks. The API may require customers to provide personal information, such as their name, address, date of birth, and ID documents, which are then compared with data from various sources.

What are the benefits of using KYC Check API?

The benefits of using KYC Check API include faster processing times, improved accuracy, reduced costs, and enhanced security.

What documents are required for KYC verification using API?

The documents required for KYC verification using API may vary depending on the provider and the country. However, customers are typically required to provide a government-issued ID document, such as a passport or driver’s license.

Is KYC Check API secure?

Yes, KYC Check API is typically secure, as it uses encryption and other security measures to protect customer data.

What are the technical requirements for integrating KYC Check API?

The technical requirements for integrating KYC Check API vary depending on the provider and the technology used. However, businesses are typically required to have a system for capturing and transmitting customer data securely.

What is the cost of using KYC Check API?

The cost of using KYC Check API varies depending on the provider and the level of service required.

Who can use KYC Check API?

Any business that is authorized to perform KYC checks can use KYC Check API. However, they must comply with applicable regulations and laws.

How reliable is KYC Check API for identity verification?

KYC Check API can be reliable for identity verification, but it is important to choose a reputable provider and ensure that the system is properly configured to meet regulatory requirements.

What are the regulatory requirements for using KYC Check API?

Businesses are required to comply with applicable regulations and laws, including data protection laws and KYC regulations.

Video KYC API

What is Video KYC API?

Video KYC API is an interface that allows businesses to perform KYC checks on their customers using video verification. The API integrates with various data sources and uses algorithms and machine learning to verify customer identities.

How does Video KYC API work?

Video KYC API works by allowing customers to complete the KYC process remotely, using a video call. The call is recorded and analyzed using AI-powered tools to verify the customer’s identity.

What are the benefits of using Video KYC API?

The benefits of using Video KYC API include faster processing times, improved accuracy, reduced costs, and enhanced security.

What are the technical requirements for integrating Video KYC API?

The technical requirements for integrating Video KYC API vary depending on the provider and the technology used. However, businesses are typically required to have a system for capturing and transmitting video securely.

Is Video KYC API secure?

Yes, Video KYC API is typically secure, as it uses encryption and other security measures to protect customer data.

What documents are required for Video KYC verification using API?

The documents required for Video KYC verification using API may vary depending on the provider and the country. However, customers are typically required to provide a government-issued ID document, such as a passport or driver’s license.

What is the cost of using Video KYC API?

The cost of using Video KYC API varies depending on the provider and the level of service required.

Who can use Video KYC API?

Any business that is authorized to perform KYC checks can use Video KYC API. However, they must comply with applicable regulations and laws.

How reliable is Video KYC API for identity verification?

Video KYC API can be reliable for identity verification, but it is important to choose a reputable provider and ensure that the system is properly configured to meet regulatory requirements.

What are the regulatory requirements for using Video KYC API?

Businesses are required to comply with applicable regulations and laws, including data protection laws and KYC regulations.

Try IDcentral’s KYX solution that uses AI-enabled KYC API for ID verification

Aadhaar Plus

Aadhaar Plus  Document Verification

Document Verification  Liveness Detection

Liveness Detection  Face Trace

Face Trace Face Match

Face Match  Government DB Check

Government DB Check  Video KYC

Video KYC  Hover Plus

Hover Plus  DeepScan

DeepScan  Identity Verification

Identity Verification AML Screening & Monitoring

AML Screening & Monitoring  Digital Onboarding

Digital Onboarding  KYX Solution

KYX Solution  Banking and Financial Services

Banking and Financial Services Telecommunication

Telecommunication  Insurance

Insurance  Gaming

Gaming Retail Services

Retail Services  Shared Economy

Shared Economy Travel

Travel  Blog

Blog Webinars

Webinars Whitepapers

Whitepapers Infographics

Infographics Identity Dictionary

Identity Dictionary Frequently Asked Questions

Frequently Asked Questions